Ravi wakes up at 4 AM every day. He loads his cart with fresh vegetables, pushes it to the local market, and earns between ₹800 and ₹1,500 a day. He has done this for 12 years. He saves regularly. He takes care of his family. And more than anything, he wants to own a home.

But when Ravi walked into a bank and asked about a home loan, the officer asked for salary slips and ITR documents. Ravi had neither. So he walked out — without a loan and without hope.

Here’s the thing though: Ravi absolutely deserves a home loan. And he can get one.

This post is for every Ravi out there — vegetable vendors, street food sellers, daily wage workers, small traders, and micro-business owners. If you earn consistently and you dream of owning a home, keep reading. Because Easy Home Finance was built specifically for people like you.

The Real Problem: Banks Built for the Wrong People

Most banks have a very narrow idea of who qualifies for a home loan. They want salary slips. They want ITR filings. They want formal employment letters. And if you don’t have these, they say no — sometimes without even looking at your actual income.

But here’s what those banks are missing. Millions of Indians earn honest, consistent incomes every single day — without a formal salary structure. In fact, according to the Periodic Labour Force Survey, over 90% of India’s workforce operates in the informal economy.

So the problem isn’t that daily earners can’t repay a loan. The problem is that traditional banks never built a system to include them.

That’s exactly where Easy Home Finance is different.

So, Can a Vegetable Vendor Actually Get a Home Loan?

Yes. Absolutely.

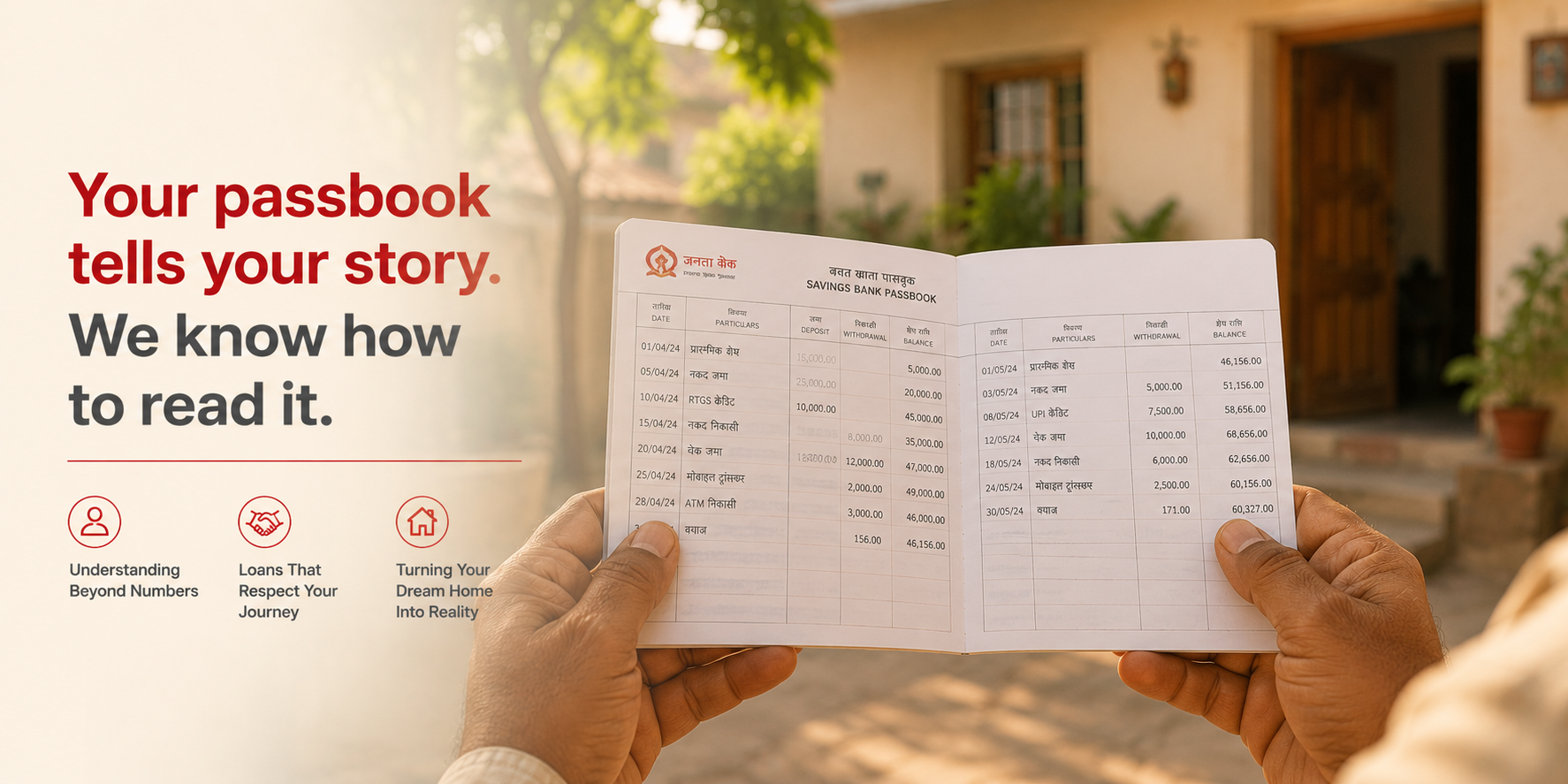

Easy Home Finance looks beyond salary slips and ITR documents. Instead, our team looks at your actual financial life — how you earn, how you save, and how you manage money every day.

Here is what matters to us:

Your daily or weekly income pattern Even if your income varies, consistency matters more than the amount. Earning ₹1,000 a day, six days a week, over several years tells a powerful story.

Your bank account activity Do you deposit money regularly? Do you save? A clean and active bank account — even a basic savings account — is a strong sign of financial discipline.

How long you have been doing this work A vegetable vendor who has been running the same stall for eight years is a reliable borrower. Stability of livelihood matters just as much as the type of livelihood.

Any assets you already own A small piece of land, gold, or any existing property can further support your loan application.

Your credit history If you have repaid any past loans — even a small Kisan Credit Card or a microfinance loan — on time, that works in your favour significantly.

What Documents Do You Need?

You don’t need a salary slip. You don’t need an ITR. However, you do need some basic paperwork. Here is a simple list:

- Identity Proof: Aadhaar card, PAN card, or Voter ID

- Address Proof: Utility bill, ration card, or rental agreement

- Bank Statements: Last 6 to 12 months from your savings account

- Income Proof: Cash memos, market association letters, or a self-declaration of income certified by a local authority

- Property Documents: Title deed or agreement to sale for the property you want to buy

- Business Proof (if available): Shop registration, market committee certificate, or trade licence

Even if you don’t have all of these, talk to our team first. We will guide you on exactly what is needed for your specific situation.

How Easy Home Finance Makes It Work

At Easy Home Finance, we follow a process that is built around your reality — not around a checklist designed for corporate employees.

First, we listen. Our loan officers are trained to understand informal income. They know what a vegetable vendor’s income looks like. They also know what a daily wage earner’s cash flow pattern typically is. So they ask the right questions instead of turning you away.

Then, we assess your real repayment ability. We calculate how much you earn on average per month. Next, we look at your fixed expenses and existing obligations. Finally, we determine what EMI you can comfortably afford. This whole process is transparent and honest.

After that, we move fast. We know that waiting months for a loan decision is frustrating. Therefore, Easy Home Finance aims to give you a clear answer quickly — so you can plan your next step with confidence.

And throughout everything, we keep it simple. No complicated jargon. No confusing paperwork trails. Just a clear, step-by-step process that respects your time and your situation.

Start your application here — it takes less than 5 minutes.

A Quick Reality Check on Loan Amounts and EMIs

You might be wondering: how big a loan can a vegetable vendor actually get?

The honest answer is — it depends on your income, your location, and the property you want to buy. However, here is a simple way to think about it:

If you earn around ₹25,000 per month on average, you could potentially qualify for a home loan of ₹10–15 lakhs, depending on your existing obligations and the property value.

Additionally, if you add a co-applicant — a working spouse or an earning family member — your combined income increases your eligibility significantly. Therefore, applying jointly is always a smart move.

Real Stories From Real Borrowers

Still unsure if this is really possible? Then watch and listen to the people who’ve already done it.

Visit our YouTube channel to hear real stories from borrowers just like you — daily earners, small traders, and first-time homeowners who thought a home loan was out of reach. It wasn’t. And it isn’t for you either.

The Bottom Line

A vegetable vendor is not less deserving of a home than a salaried professional. Moreover, consistent daily earnings are just as real as a monthly salary — they simply look different on paper.

Easy Home Finance exists to bridge exactly that gap. We believe that your hard work — however informal — should be enough to build a home for your family.

So if you wake up early, work hard, and save whatever you can, you deserve a fair shot at homeownership. And we are here to give you that shot.

Apply for a home loan today — no salary slip, no ITR needed.

You built your livelihood from scratch. Now let’s build your home.

Frequently Asked Questions

Can a vegetable vendor or daily wage earner qualify for a home loan? Yes. Easy Home Finance offers home loans to daily earners, small traders, and informal sector workers. We assess your income based on bank statements, cash flow patterns, and work history — not just formal salary documents. Apply here to check your eligibility.

What proof of income is accepted if I don’t have salary slips? Lenders like Easy Home Finance accept alternatives such as bank statements, cash memos, self-declaration of income, market association letters, GST returns, and Chartered Accountant certificates. The key is showing consistent and regular earnings over time.

How much home loan can an informal worker get? It depends on your average monthly income, existing liabilities, and the property value. As a general rule, your EMI should not exceed 40–50% of your monthly income. Adding a co-applicant can increase your eligible loan amount significantly.

Do I need a good CIBIL score to get a home loan without formal income proof? A good CIBIL score — ideally above 700 — strengthens your application considerably. However, if you have limited credit history, Easy Home Finance evaluates other factors such as savings behaviour, bank activity, and income consistency.

How do I get started with Easy Home Finance? Simply fill out our short online application or reach out to our team directly. We will assess your profile, explain your options clearly, and guide you through every step — in plain, simple language.

Leave a Comment