Rickshaw Drivers Deserve a Real Home Loan — And Here’s How to Get One

Suresh has been driving his auto-rickshaw for eleven years. Every morning he starts his engine before sunrise. Every evening he comes home tired — but with cash in hand. He has never missed rent. He has never borrowed money he couldn’t repay. And for the last five years, he has been quietly saving for a home of his own.

But every bank told him the same thing. No salary slip. No ITR. No loan.

That answer is wrong. And it is unfair.

Auto-rickshaw and taxi drivers are among the most hardworking, financially disciplined earners in India. Therefore, they absolutely deserve a fair shot at a home loan. This guide will show you exactly how to get one — step by step, in plain language.

Why Drivers Struggle to Get a Home Loan From Regular Banks

Most traditional banks have a very rigid lending system. They are designed for salaried employees who receive a fixed monthly salary into a bank account. As a result, they ask for salary slips, Form 16, and Income Tax Returns.

Auto-rickshaw and taxi drivers earn daily. Their income comes in cash. It varies by season and by day. And most of them do not file ITR because their annual income may fall below the taxable threshold or because they simply don’t know they should.

However — and this is important — none of that means they cannot repay a loan. It simply means their income looks different on paper. Traditional banks have not built systems to understand that difference. But Easy Home Finance has.

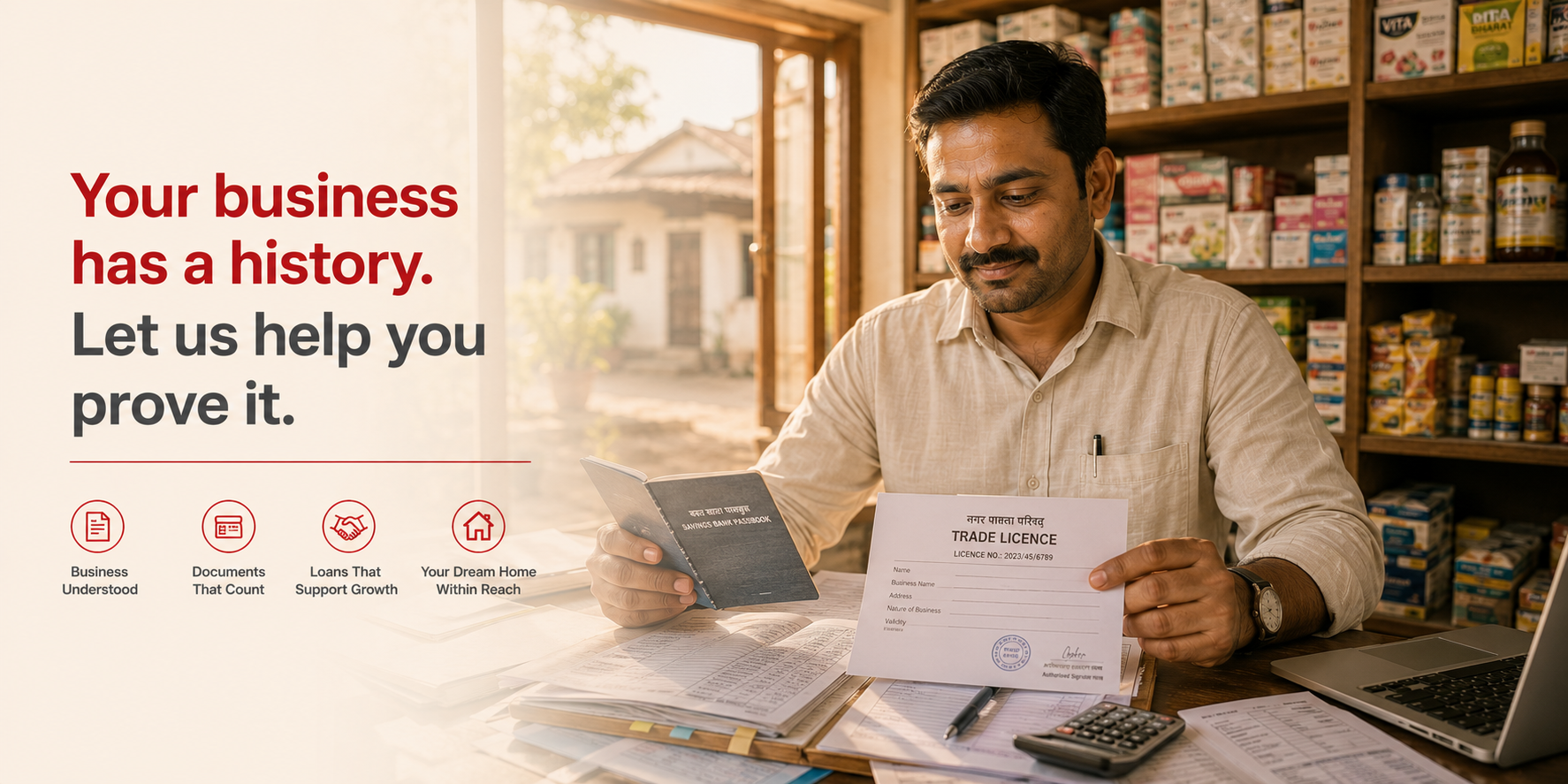

What Documents Does a Driver Actually Need?

You do not need a salary slip. You do not need an ITR. However, you do need to show some paperwork that tells your financial story. Here is a practical list:

Identity and Address

- Aadhaar card, PAN card, or Voter ID

- Utility bill, ration card, or rental agreement for address proof

Income and Work Proof

- Bank statements for the last 6 to 12 months — this is the most important document

- Driving licence (commercial)

- Vehicle permit or route permit

- Vehicle RC (Registration Certificate)

- Badge card issued by the Regional Transport Office (RTO)

Financial History

- Any existing loan repayment records — vehicle loan, microfinance loan, or Kisan Credit Card

- Your CIBIL score report — ideally 650 or above

Property Documents

- Agreement to sale, title deed, or builder’s allotment letter for the property you want to buy

Even if you are missing a document or two, do not let that stop you. Reach out to our team first and we will help you understand exactly what works for your specific situation.

How Easy Home Finance Assesses a Driver’s Income

At Easy Home Finance, we understand that daily cash income is real income. Therefore, our team is trained to assess informal earners fairly. Here is what we actually look at:

Your Bank Statement Pattern Do you deposit money regularly — even small amounts, multiple times a week? Consistent deposits across 6 to 12 months show us your earning rhythm clearly. This is the single most powerful document you can bring.

How Long You Have Been Driving A driver with 8 to 10 years of experience has demonstrated occupational stability. Moreover, an RTO badge or permit that has been renewed consistently is strong proof of livelihood continuity.

Your Vehicle Loan Repayment Most auto-rickshaw and taxi drivers have taken a vehicle loan at some point. If you have repaid it on time — or are currently repaying it — that directly improves your CIBIL score and proves repayment discipline.

Your Route or Area of Operation Drivers who operate in high-demand urban or semi-urban areas often have more predictable daily earnings. Additionally, those affiliated with aggregator platforms like Ola or Uber have digital trip and earnings records that can serve as supporting income proof.

Any Co-Applicant Income If your spouse earns — even informally — adding them as a co-applicant increases your combined eligibility. This is often the smartest move for a driver applying for a joint home loan.

A Smart Step Before You Apply: Get Your Bank Statement Right

Here is one practical tip that most people miss. Start depositing your daily earnings into your bank account regularly — even if you later withdraw cash for expenses.

Why does this matter? Because your bank statement becomes your income proof. A statement that shows regular daily or weekly credits — even of varying amounts — builds a picture of consistent earnings. Over 6 to 12 months, this becomes one of the strongest documents you can submit.

Therefore, if you are planning to apply for a home loan in the next year, start building this habit today. It costs you nothing and significantly improves your application.

How the Easy Home Finance Process Works

We keep everything simple and human. Here is what happens when you apply:

Step 1 — Apply Online in Minutes Fill out a short form on our website. It takes less than five minutes. Start here.

Step 2 — We Call You A member of our team will call you to understand your work, income, and the kind of home you are looking for. There is no judgement and no jargon in this conversation.

Step 3 — We Guide You on Documents We tell you exactly which documents work for your profile. We do not ask for what you cannot provide. Instead, we work with what you have.

Step 4 — We Assess Your Application Our credit team looks at your full profile — your bank statement, work history, repayment record, and property details. Then we give you a clear and transparent assessment.

Step 5 — Sanction and Support Once approved, we guide you through the remaining steps clearly. Our goal is to make the process feel manageable — not overwhelming.

Watch real stories from borrowers like you on our YouTube channel.

Tips to Improve Your Home Loan Chances Right Now

Even before you apply, there are things you can do to strengthen your profile:

Maintain a clean CIBIL score Pay your existing vehicle loan, credit card, or any other EMI on time — every single month. Even one missed payment affects your score negatively. Check your CIBIL score for free here.

Keep your bank account active Deposit your daily earnings regularly. Avoid long gaps in account activity. A consistently active account tells a strong story to any lender.

Renew your permits and licence on time An up-to-date driving licence, vehicle permit, and RTO badge are not just legal requirements — they are also proof of your professional seriousness. Keep all renewals current.

Avoid multiple loan applications at once Each time you apply for a loan and the lender does a hard credit inquiry, it slightly reduces your CIBIL score. Therefore, apply thoughtfully — not everywhere at once.

Consider applying jointly If your spouse or a family member earns any income, apply together. Combined income means higher eligibility and a stronger overall application.

The Bottom Line

Auto-rickshaw and taxi drivers are among India’s most dependable earners. They show up every day, in every kind of weather, and they keep cities moving. Therefore, they deserve a home loan system that shows up for them in return.

Easy Home Finance was built to do exactly that. We look at your real income, your real work history, and your real repayment ability — not just what fits into a bank’s checklist.

Here is what to remember:

- Regular bank deposits are your most powerful income proof

- Commercial driving licence, vehicle permit, and RTO badge all support your application

- A good CIBIL score and vehicle loan repayment history work strongly in your favour

- Applying jointly with a co-applicant increases your eligible loan amount

- Easy Home Finance assesses informal income fairly and transparently

You have driven through every challenge life has given you. Now let us help you drive home.

Apply for your home loan today — no salary slip needed.

You built your livelihood on the road. Now let’s build your home off it.

Frequently Asked Questions

Can an auto-rickshaw or taxi driver get a home loan in India? Yes. Lenders like Easy Home Finance offer home loans to drivers and other informal earners. We assess your income through bank statements, commercial driving licence, vehicle permit, RTO badge, and repayment history — not salary slips. Check your eligibility here.

What is the most important document for a driver applying for a home loan? Your bank statement for the last 6 to 12 months is the single most important document. Regular deposits — even of varying daily amounts — demonstrate consistent income far more clearly than any single certificate.

Does an Ola or Uber driver have any advantage in getting a home loan? Yes, potentially. Aggregator platform drivers have access to digital trip records and weekly earnings summaries through the app. These records can serve as supporting income proof alongside bank statements. Talk to our team to understand how your platform records can be used.

What CIBIL score does a driver need to qualify for a home loan? A CIBIL score of 650 or above is generally helpful. If you have repaid a vehicle loan on time, that history already contributes positively to your score. Easy Home Finance considers your full financial profile — not just the score in isolation.

Can I apply for a joint home loan with my spouse if we both earn informally? Yes. Applying jointly combines both incomes and increases your total loan eligibility. Even if both incomes are informal or cash-based, Easy Home Finance assesses them together through bank statements and alternative documents. Apply jointly here.

Leave a Comment