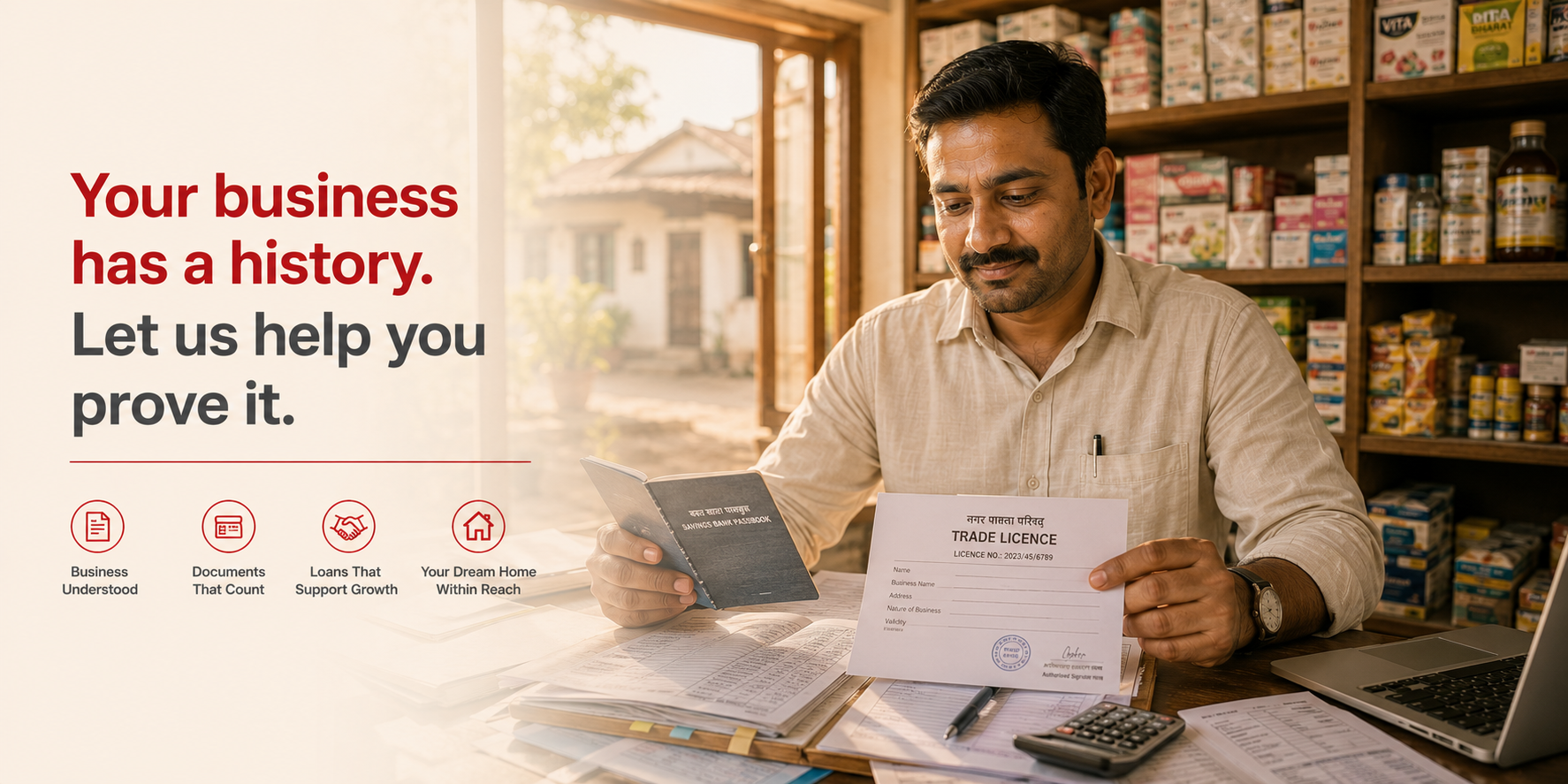

Can a Kirana Owner Finally Get a Home Loan? Yes — Here’s How

Mahesh has run the same kirana shop for fourteen years. He opens at 7 AM and closes at 10 PM. He knows every customer by name. His shop feeds six families in the building next door. And every month, without fail, he puts aside a small amount toward one dream — owning a home.

But every bank he walked into gave him the same answer. No ITR filed regularly. No salary slip. No formal income proof. No loan.

That answer is deeply unfair. And fortunately, it is not the only answer available anymore.

Shop owners, kirana traders, small business owners — they are among India’s most resilient earners. Therefore, they deserve a home loan system that actually works for them. This guide will show you exactly how to get a home loan as a small trader — clearly, practically, and without confusion.

Why Banks Keep Saying No to Shop Owners

Traditional banks were designed for one type of borrower — a salaried employee with a fixed monthly income, a salary slip, and a Form 16 from their employer. If you fit that mould, the process is smooth. But if you don’t, the system stops working very quickly.

Small traders and shop owners earn differently. Income varies by season, by festival, by footfall, and sometimes by weather. Many kirana owners mix personal and business expenses. Some file GST returns but not ITR. Others do neither, simply because no one ever explained why they should.

However, none of this means they cannot repay a loan. In fact, a shop owner who has survived for ten years in a competitive market has demonstrated far more financial resilience than most salaried employees. Traditional banks just don’t have the tools to see that. Easy Home Finance does.

What Documents Do Shop Owners Actually Need?

You do not need three years of clean ITR. However, you do need to show some documentation that gives a lender a clear picture of your financial life. Here is a practical checklist:

Identity and Address Proof

- Aadhaar card, PAN card, or Voter ID

- Utility bill, ration card, or shop rental agreement as address proof

Business Existence Proof

- Shop and Establishment Registration Certificate

- GST registration certificate (if registered under GST)

- Trade licence issued by your local municipal authority

- Udyam Registration Certificate if you are registered as an MSME under the Ministry of MSME

Income and Financial Proof

- Bank statements for the last 6 to 12 months — both personal and business accounts if separate

- GST returns for the last 6 to 12 months (if applicable)

- CA-certified income statement or net worth certificate

- Business receipts, purchase invoices, or stock records

Property Documents

- Agreement to sale, title deed, or allotment letter for the property you want to buy

Even if you are missing some of these, do not stop there. Reach out to our team first and we will guide you on exactly what is workable for your situation.

How Easy Home Finance Reads a Trader’s Income

At Easy Home Finance, we understand that a shop owner’s income statement looks very different from a payslip. Therefore, we have built our assessment process specifically to evaluate informal and self-employed borrowers fairly.

Here is what we actually look at:

Bank Statement Activity This is your most powerful document. Regular credits — even of varying amounts — over 6 to 12 months tell us the rhythm of your business income. Consistent deposits show financial discipline, regardless of whether the amounts are fixed.

GST Returns as Turnover Proof If you file GST returns, those filings are an excellent proxy for your business turnover. According to the GST Council of India, over 1.4 crore businesses filed GST returns regularly as of recent years. If you are one of them, that record works strongly in your favour.

Business Vintage How long have you been running your shop? A kirana store that has operated at the same location for eight years demonstrates occupational stability and community trust. We treat that seriously.

Udyam / MSME Registration If you are registered under the Udyam portal as a micro or small enterprise, that registration itself is a credible indicator of your business’s legitimacy and continuity.

Existing Loan Repayment Behaviour Have you repaid a business loan, a gold loan, or any previous borrowing on time? Your CIBIL score reflects this. A score of 650 or above strengthens your application considerably. Even a modest repayment history shows us how you handle financial obligations.

Co-Applicant Income If your spouse or a family member earns any income — formal or informal — adding them as a co-applicant increases your combined eligibility and overall application strength.

A Practical Tip That Most Shop Owners Miss

Many kirana owners maintain two cash flows — one through the bank and one in hand. As a result, their bank statement looks smaller than their actual income.

Here is one thing you can do right now, even before applying. Start channelling more of your daily sales through your bank account. Deposit earnings regularly, even if you withdraw later for expenses. Over 6 to 12 months, this creates a visible income trail that becomes your most credible income document.

This single habit can significantly improve your loan eligibility. It costs you nothing and builds a foundation that any lender — including traditional banks — will find difficult to ignore.

GST Registration: Should You Register Before Applying?

If your annual turnover exceeds ₹40 lakhs (₹20 lakhs for service providers), GST registration is mandatory under the GST Act. However, even if you are below the threshold, voluntary registration is possible and beneficial.

Having GST returns on record adds credibility to your income claims and provides a lender with a consistent, government-verified picture of your business. Therefore, if you are planning to apply for a home loan in the next 12 to 18 months, speaking to a CA about voluntary GST registration is worth considering.

How the Easy Home Finance Process Works

We keep the entire process simple and human. Here is what happens when you apply:

Step 1 — Apply in Minutes Fill out our quick online form. It takes less than five minutes. Start here.

Step 2 — We Call You A member of our team calls you to understand your shop, your income pattern, and what kind of home you are looking for. No jargon. No judgement.

Step 3 — We Identify Your Documents We tell you exactly which documents work for your specific profile. We do not ask for what you cannot provide. Instead, we work with what is available.

Step 4 — We Assess Your Full Profile Our credit team reviews your bank statements, business proof, GST records, repayment history, and property details together — as a full picture, not a checklist.

Step 5 — Clear Answer, Fast We move quickly because we know waiting is frustrating. Our goal is to give you a transparent decision so you can plan your next step with confidence.

Watch real stories from borrowers like you on our YouTube channel.

Things You Can Do Right Now to Strengthen Your Application

You do not need to wait until you apply to start improving your profile. Here are steps you can take today:

Deposit earnings regularly Make it a habit to deposit a portion of your daily or weekly sales into your bank account consistently. Over time, this builds a strong income trail.

Keep your CIBIL score healthy Pay any existing loans, credit card bills, or EMIs on time — every single month. Even one missed payment negatively impacts your score. Check your CIBIL score for free here.

Get your business registered If you have not already, register your business under the Udyam portal. It is free, quick, and immediately adds credibility to your profile. Register here.

File GST returns consistently If you are already registered under GST, ensure your returns are filed on time and accurately. Consistency matters far more than the turnover amount.

Separate your personal and business accounts If you currently use one account for both personal and business transactions, opening a separate current account for your business makes your income far easier to assess.

The Bottom Line

Kirana owners and small traders are the backbone of India’s local economy. According to the Retailers Association of India, there are over 1.3 crore kirana stores operating across the country. These are real businesses, run by real people, with real and consistent incomes.

Therefore, they deserve a home loan system that sees them clearly. Easy Home Finance was built to do exactly that. We look at your full financial picture — your bank statements, business records, GST filings, and repayment history — and we make a fair assessment based on your actual ability to repay.

Here is what to remember:

- Bank statements are your most powerful income proof — start building them today

- GST returns, Udyam registration, and trade licences all strengthen your application

- A CIBIL score of 650 or above significantly improves your eligibility

- Adding a co-applicant increases your combined loan amount

- Easy Home Finance evaluates informal and self-employed income fairly

You built your shop with discipline and dedication. Now let us help you build your home.

Apply for your home loan today — no ITR or salary slip needed.

Your shop has been your foundation for years. Now let’s make it the foundation of something bigger.

Frequently Asked Questions

Can a kirana shop owner or small trader get a home loan in India? Yes. Easy Home Finance offers home loans to self-employed individuals and small business owners. We assess income through bank statements, GST returns, business registration documents, and CA certificates — not just ITR or salary slips. Check your eligibility here.

What is the most important document for a shop owner applying for a home loan? Your bank statement for the last 6 to 12 months is the single most important document. Regular deposits — even if amounts vary — show a consistent earning pattern that lenders can assess clearly and confidently.

Does GST registration help in getting a home loan? Yes, significantly. GST returns provide a government-verified record of your business turnover. Consistent GST filings over 6 to 12 months serve as strong supporting income proof. If you are not yet registered and your turnover qualifies, speaking to a CA about registration before applying is a smart move.

What CIBIL score does a small trader need for a home loan? A CIBIL score of 650 or above is generally helpful and strengthens your application. If you have repaid any previous business loan, gold loan, or other borrowing on time, that history already contributes positively. Easy Home Finance reviews your full profile, not just the number.

Can I apply jointly with my spouse if we both earn from the same shop? Yes. Applying jointly combines both incomes and increases your total loan eligibility. Even if both incomes come from the same business, Easy Home Finance assesses the combined household repayment capacity. Apply jointly here.

Leave a Comment