Signing a home loan agreement is a big step. In fact, it is one of the most important documents you will ever sign. Yet most people skim through it. So before you pick up that pen, take a few minutes to read this first.

Why Reading the Agreement Matters

A home loan runs for 10, 20, or even 30 years. As a result, even a small error in the agreement can cost you a lot of money. Moreover, once you sign, changes are very hard to make. So it always pays to read carefully.

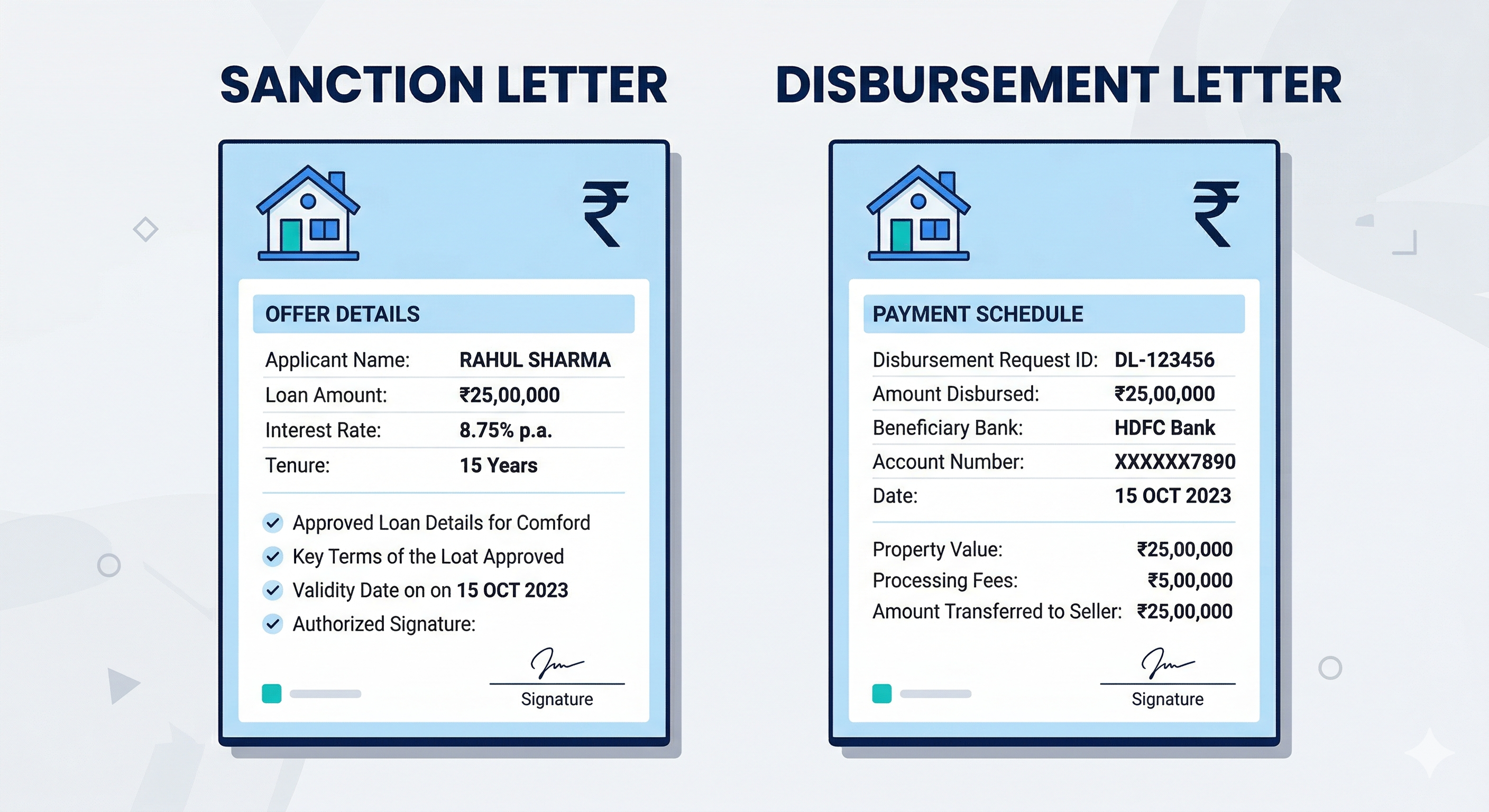

1. Check the Loan Amount

First, confirm the loan amount is correct. Make sure it matches what your home finance company approved in the sanction letter. Even a small mismatch can cause problems later.

2. Look at the Interest Rate

Next, check whether your rate is fixed or floating. A fixed rate stays the same. A floating rate changes with the market. Also, confirm the exact percentage. Even a 0.5% difference matters a lot over 20 years.

3. Read the EMI Details

Your EMI amount should be clearly stated. In addition, check the EMI start date. Many borrowers are surprised to find EMIs start earlier than expected. So use an EMI calculator beforehand to know your exact number.

4. Check the Loan Tenure

Look at the number of years for repayment. Furthermore, check if the tenure matches what you agreed on verbally. A longer tenure means lower EMIs but more interest overall. So choose wisely.

5. Look for Hidden Charges

This is a step most people skip. However, it is very important. Watch out for:

- Processing fees — charged when you apply

- Prepayment charges — fees if you repay early

- Late payment penalty — charged if you miss an EMI

- Conversion charges — if you switch from fixed to floating rate

Ask your home loan finance company to explain any charge you do not understand.

6. Understand the Foreclosure Terms

Foreclosure means paying off your loan early. As a result, you save on interest. However, some lenders charge a fee for this. Therefore, always check the foreclosure clause before signing.

7. Read the Default Clause

This tells you what happens if you miss payments. For instance, how many missed EMIs lead to a legal notice? What are the consequences? Knowing this helps you plan better and avoid stress later.

8. Verify Your Personal Details

Finally, check all your personal information. Look at your name, address, PAN number, and property details. Even a small typo can delay your disbursement. So take two minutes to verify everything carefully.

A Quick Checklist Before You Sign

| What to Check | Done? |

|---|---|

| Loan amount matches sanction letter | ✓ |

| Interest rate is correct | ✓ |

| EMI amount and start date | ✓ |

| Loan tenure is right | ✓ |

| All fees and charges listed | ✓ |

| Foreclosure terms are clear | ✓ |

| Default clause understood | ✓ |

| Personal details are correct | ✓ |

One Last Tip

Never feel rushed to sign. A good housing finance partner will always give you time to read. If something is unclear, ask. If something feels wrong, speak up. Above all, remember — this is your home loan. You have every right to understand it fully before you commit.

Explore More Home Loan Resources

Knowledge Hub

Read more guides on home loans, mortgage loans, and property financing.

https://easyhomefinance.in/knowledge-hub/

Apply for a Home Loan Online

Start your home loan application easily.

https://easyhomefinance.in/

Home Loan EMI Calculator

Estimate your monthly repayment before applying for a home loan.

https://easyhomefinance.in/emi-calculator/

Home Loan Solutions

Explore housing finance options designed for first-time buyers and self-employed borrowers.

https://easyhomefinance.in/home-loans/

Leave a Comment